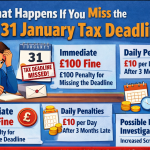

What happens if you miss the 31 January tax deadline?

December 30, 2025

Can You Really “Backdate” Expenses? What HMRC Allows

January 4, 2026

Director’s Loan Accounts (DLAs) are useful for owner-managed businesses, but they are also one of the most common areas where mistakes lead to unexpected tax bills. HMRC pays close attention to DLAs, and small errors can quickly result in corporation tax charges, personal tax liabilities, and penalties.

Below are the most common Director’s Loan Account mistakes we see, and how they can trigger tax charges.

1. Taking Money Without Understanding the Director’s Loan Account

A Director’s Loan Account records money taken out of a company by a director that is not salary, dividends, or reimbursed expenses. Many directors withdraw funds casually, assuming it can be sorted later.

If the loan account becomes overdrawn and is not repaid within the required time limits, it can create both company and personal tax charges.

2. Not Repaying the Loan Within 9 Months of Year End

If a director owes money to the company more than 9 months and 1 day after the accounting year end, the company may face a Section 455 tax charge.

This charge is currently 33.75 % of the outstanding loan balance. Although this tax can be reclaimed once the loan is repaid, it can take time and affects company cash flow.

Many directors assume repayment can wait, only to discover the charge when accounts are finalised.

3. Clearing the Loan With Dividends That Are Not Legal

Using dividends to clear a Director’s Loan Account is common, but dividends can only be declared if the company has sufficient distributable reserves.

Declaring dividends without profits is illegal and can lead to HMRC challenges, reclassification of payments, and additional tax.

4. Using Director’s Loan Accounts for Personal Expenses

Paying personal bills through the company, such as household costs or private purchases, often ends up posted to the Director’s Loan Account.

If this becomes routine, HMRC may argue the withdrawals are disguised remuneration or benefits, which can result in income tax and National Insurance charges.

5. Not Charging Interest on Large or Long-Term Loans

If a director owes a significant amount for a long period and no interest is charged, HMRC may treat the loan as a beneficial loan.

This can create a benefit in kind, resulting in personal tax for the director and Class 1A National Insurance for the company.

6. Bed and Breakfasting the Loan Account

Some directors repay the loan briefly just before the 9-month deadline and then withdraw the funds again shortly after.

HMRC has anti-avoidance rules to prevent this. If more than £5,000 is repaid and borrowed again within 30 days, the loan is treated as never having been repaid, and the Section 455 charge can still apply.

7. Poor Record Keeping and Late Accounting

Director’s Loan Accounts rely on accurate and up-to-date bookkeeping. Late posting of transactions, missing expense claims, or unclear dividend records often cause the loan balance to be wrong.

Incorrect balances can lead to unexpected tax charges being discovered too late to fix them efficiently.

8. Assuming the Company and Personal Tax Are Separate

Many directors forget that Director’s Loan Accounts affect both company tax and personal tax.

An overdrawn loan can trigger corporation tax, benefit in kind charges, and additional income tax for the director, all at the same time.

How to Avoid Director’s Loan Account Tax Charges

The best way to avoid tax charges is proactive planning. This includes understanding how money is taken from the company, reviewing loan balances regularly, declaring dividends properly, and repaying loans within the required time limits.

Director’s Loan Accounts should be reviewed throughout the year, not just when accounts are prepared.

Need Help With a Director’s Loan Account?

If you are unsure whether your Director’s Loan Account is overdrawn, or you want to avoid Section 455 or benefit in kind charges, it is best to take advice early.

At Taxes Done Right, we help directors structure drawings properly, stay compliant, and avoid unnecessary tax bills.

{kind=link}

{kind=link}

{kind=link}