The 12-Month VAT Test Explained: When Do You Need to Register for VAT?

June 23, 2026

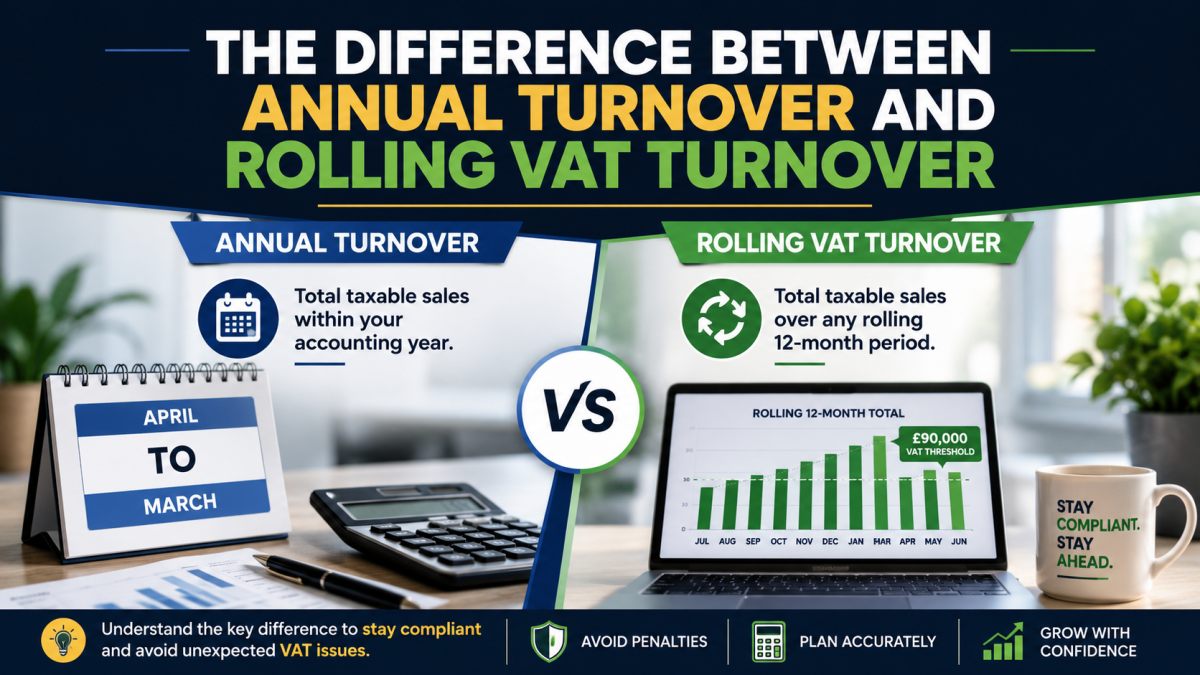

The Difference Between Annual Turnover and Rolling VAT Turnover

Annual Turnover and Rolling VAT Turnover are two important financial measurements that every UK business owner should understand. Although they may sound similar, they serve very different purposes, particularly when it comes to VAT registration and HMRC compliance.

Many businesses mistakenly monitor only their annual turnover figures, believing this is sufficient for VAT purposes. However, HMRC uses a rolling 12-month calculation when assessing whether a business has exceeded the VAT registration threshold. Understanding the distinction can help businesses avoid costly penalties, late registration issues, and unexpected VAT liabilities.

What Is Annual Turnover?

Annual turnover refers to the total income generated by a business during a specific accounting period, typically a financial year. It includes all sales and revenue before expenses are deducted.

Businesses commonly use annual turnover to:

- Measure overall business performance

- Prepare annual accounts

- Assess growth year on year

- Support loan and finance applications

- Compare financial results between accounting periods

For example, if a business generates £120,000 of sales between 1 April 2025 and 31 March 2026, its annual turnover for that accounting year would be £120,000.

While annual turnover is important for financial reporting, it is not the method HMRC uses when determining whether a business should register for VAT.

Annual Turnover and Rolling VAT Turnover: The Key Difference

The main difference between Annual Turnover and Rolling VAT Turnover is the period being measured.

Annual turnover looks at a fixed accounting period, usually a financial year.

Rolling VAT turnover continuously measures taxable turnover over the previous 12 months and is recalculated every month.

This means that a business can exceed the VAT registration threshold even if its annual turnover appears lower when viewed by accounting year.

HMRC requires businesses to review their taxable turnover at the end of every month and calculate the total taxable sales made during the preceding 12-month period.

This rolling calculation is what determines whether VAT registration becomes mandatory.

What Is Rolling VAT Turnover?

Rolling VAT turnover is the total value of taxable sales made during the most recent 12 months.

Unlike annual turnover, there is no fixed start or end date.

Each month, the oldest month drops out of the calculation and the newest month is added.

For example:

- At the end of June, review turnover from July of the previous year to June.

- At the end of July, review turnover from August of the previous year to July.

- At the end of August, review turnover from September of the previous year to August.

This process continues every month.

Because of this rolling approach, businesses experiencing rapid growth can cross the VAT threshold unexpectedly if they are not actively monitoring turnover.

Why HMRC Uses Rolling VAT Turnover

HMRC uses rolling VAT turnover because it provides a more accurate reflection of a business’s recent trading activity.

A business may experience periods of rapid growth, seasonal fluctuations, or significant increases in sales. Using a rolling calculation allows HMRC to identify when a business has genuinely reached a level where VAT registration becomes necessary.

This system helps ensure that businesses register at the correct time rather than delaying registration until the end of an accounting year.

Failure to monitor rolling VAT turnover can result in:

- Late VAT registration

- Backdated VAT liabilities

- Interest charges

- HMRC penalties

- Increased administrative costs

Annual Turnover and Rolling VAT Turnover Example

Consider a business with the following taxable sales:

| Month | Sales |

|---|---|

| January | £6,000 |

| February | £7,000 |

| March | £7,500 |

| April | £8,000 |

| May | £8,500 |

| June | £9,000 |

| July | £9,500 |

| August | £10,000 |

| September | £10,500 |

| October | £11,000 |

| November | £11,500 |

| December | £12,000 |

The business may not initially realise it is approaching the VAT threshold because individual monthly sales appear manageable.

However, when these figures are added together as a rolling 12-month total, the business may exceed the VAT registration threshold, triggering a legal obligation to register for VAT.

This example highlights why monitoring rolling turnover is far more important for VAT compliance than simply reviewing annual accounts.

How Businesses Can Monitor Rolling VAT Turnover

To avoid VAT registration issues, businesses should:

Maintain Accurate Bookkeeping

Up-to-date records make it easier to identify trends and monitor taxable turnover throughout the year.

Review Turnover Monthly

Businesses should calculate their rolling VAT turnover at the end of every month rather than waiting until year end.

Understand What Counts Towards VAT Turnover

Most taxable sales count towards the VAT threshold, including standard-rated, reduced-rated, and zero-rated supplies.

Use VAT Monitoring Tools

Many accounting software packages provide VAT turnover reports that automatically calculate rolling totals.

Seek Professional Advice

If turnover is approaching the VAT threshold, professional advice can help determine registration requirements and identify planning opportunities.

Our VAT Turnover Calculator

Our free VAT Turnover Calculator helps you quickly check whether your business is approaching the VAT registration threshold. Simply enter your monthly turnover figures and instantly see your rolling 12-month taxable turnover, helping you stay compliant and avoid unexpected VAT registration obligations.

Final Thoughts

Understanding the difference between Annual Turnover and Rolling VAT Turnover is essential for every business owner. While annual turnover helps measure business performance over a financial year, rolling VAT turnover is the figure HMRC uses when assessing VAT registration obligations.

Businesses that monitor only annual turnover risk missing the VAT registration threshold and facing unnecessary penalties. By reviewing turnover monthly and understanding how the rolling 12-month calculation works, business owners can remain compliant, avoid unexpected costs, and make informed decisions as their business grows.

Regular monitoring of rolling VAT turnover is one of the simplest yet most effective ways to stay on top of VAT obligations and protect the long-term success of your business.

Need help deciding what’s best for your situation?

📞 Call 0161 710 1901

📧 Email Tax@TaxesDoneRight.co.uk

Visit www.taxesdoneright.co.uk

{kind=link}

{kind=link}

{kind=link}