ICO Registration: Do Landlords Need ICO Registration in the UK?

June 18, 2026

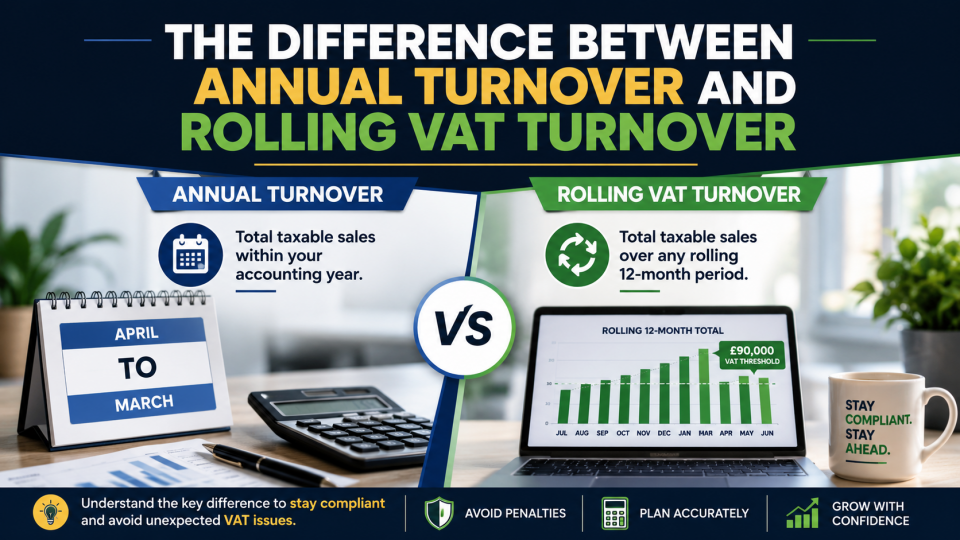

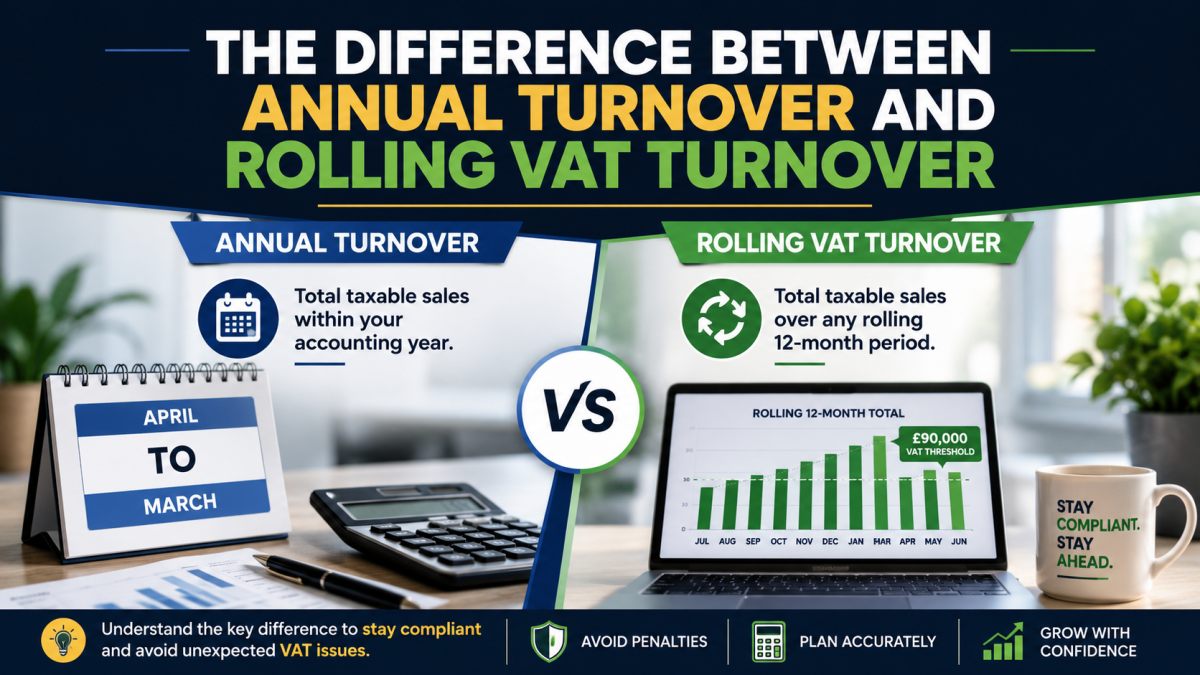

The Difference Between Annual Turnover and Rolling VAT Turnover

June 25, 2026

The 12-Month VAT Test Explained: When Do You Need to Register for VAT?

12-Month VAT Test: Understanding Your VAT Registration Obligations

The 12-Month VAT Test is one of the most important rules that UK business owners need to understand. Many people mistakenly believe that VAT registration is based on turnover within a tax year or accounting year. However, HMRC uses a rolling calculation that looks at the previous 12 months at any given point in time.

Failing to monitor the 12-Month VAT Test can result in late VAT registration, unexpected VAT liabilities, penalties, and interest charges. Whether you are a sole trader, partnership, or limited company, understanding how the test works can help you stay compliant and avoid costly mistakes.

What Is the 12-Month VAT Test?

The 12-Month VAT Test is a rolling assessment of your VAT taxable turnover over the previous 12 months. Rather than looking at a fixed accounting period, HMRC requires businesses to review their turnover at the end of every month.

If your VAT taxable turnover exceeds the VAT registration threshold during the previous 12-month period, you may be required to register for VAT.

For example, if your turnover from July 2025 to June 2026 exceeds the VAT threshold, you cannot simply wait until the end of the tax year. The obligation arises as soon as the rolling 12-month total exceeds the threshold.

This is why many growing businesses find themselves caught out. They monitor annual turnover but forget to review their turnover on a monthly rolling basis.

How the 12-Month VAT Test Works in Practice

The easiest way to understand the 12-Month VAT Test is through an example.

Imagine a business generated the following taxable sales:

- July 2025 to December 2025: £40,000

- January 2026 to March 2026: £25,000

- April 2026 to June 2026: £28,000

At the end of June 2026, the business reviews its previous 12 months of taxable turnover.

Total turnover:

£40,000 + £25,000 + £28,000 = £93,000

If this exceeds the VAT registration threshold in force at the time, the business would need to notify HMRC and register for VAT.

The key point is that the test looks backwards over the previous 12 months, not forwards and not based on an accounting year.

What Counts Towards the 12-Month VAT Test?

When applying the 12-Month VAT Test, you must include VAT taxable turnover.

This generally includes:

- Standard-rated sales

- Reduced-rated sales

- Zero-rated sales

- Certain business-related supplies

Many business owners incorrectly assume that only sales subject to VAT count towards the threshold. In reality, zero-rated sales are still taxable supplies and normally count towards VAT registration calculations.

However, some exempt income may not count towards the threshold. Examples can include certain financial services, insurance-related activities, and some educational or healthcare services.

The treatment can vary depending on your circumstances, so it is important to seek professional advice if your business has mixed income streams.

Monitoring the 12-Month VAT Test Every Month

A common mistake is checking turnover only once a year.

The 12-Month VAT Test should ideally be reviewed at the end of every month. Businesses experiencing rapid growth should monitor their figures even more closely.

A simple spreadsheet can help track:

- Monthly taxable turnover

- Rolling 12-month turnover

- Distance from the VAT threshold

- Expected future growth

Cloud accounting software such as FreeAgent, Xero, or QuickBooks can also assist with monitoring turnover trends.

Regular monitoring ensures you identify registration requirements early rather than discovering them months later when penalties may already apply.

What Happens If You Exceed the VAT Threshold?

If the 12-Month VAT Test shows that your turnover has exceeded the threshold, you generally need to notify HMRC within the required timeframe.

Your effective VAT registration date will usually be based on the rules applicable to mandatory registration.

Once registered, you will typically need to:

- Charge VAT on applicable sales

- Submit VAT returns

- Maintain VAT records

- Comply with Making Tax Digital requirements

Many businesses worry about VAT registration because it can affect pricing and cash flow. However, VAT registration can also provide benefits, including the ability to reclaim VAT on eligible business expenses.

Try Our Rolling VAT Turnover Tracker for Small Businesses

If you’re concerned about monitoring your VAT registration position, our VAT Turnover Calculator for Small Businesses can help. Simply enter your monthly turnover figures and the tool automatically calculates your rolling 12-month total, highlighting whether you are approaching or exceeding the £90,000 VAT threshold. It’s ideal for sole traders, landlords, and small businesses looking to stay compliant, monitor VAT registration obligations, and keep accurate turnover records throughout the year.

Future Turnover and the Separate Forward-Looking Test

It is important not to confuse the 12-Month VAT Test with the future turnover test.

The rolling test looks backwards over the previous 12 months.

The future test applies where you expect your taxable turnover to exceed the VAT threshold within the next 30 days alone. This can occur when a business secures a large contract or receives a significant order.

In these situations, VAT registration may become necessary even if the rolling 12-month turnover has not yet exceeded the threshold.

Understanding both tests is essential for complete VAT compliance.

Common Mistakes Businesses Make

Many businesses encounter problems because they:

- Assume VAT registration is based on a tax year

- Fail to track rolling turnover monthly

- Exclude zero-rated sales incorrectly

- Ignore future contracts that trigger registration

- Delay notifying HMRC after exceeding the threshold

These mistakes can result in backdated VAT liabilities and penalties.

Professional advice can often identify registration requirements before problems arise.

Conclusion

The 12-Month VAT Test is a rolling calculation that requires businesses to monitor their taxable turnover continuously rather than annually. By reviewing turnover each month and understanding what counts towards the threshold, business owners can avoid late registration and remain compliant with HMRC requirements.

If your turnover is approaching the VAT threshold or you are unsure whether particular income counts towards the calculation, obtaining professional advice can help you make informed decisions and avoid unnecessary costs. Keeping a close eye on the 12-Month VAT Test is one of the simplest ways to stay on top of your VAT obligations and support the long-term growth of your business.

Need help deciding what’s best for your situation?

📞 Call 0161 710 1901

📧 Email Tax@TaxesDoneRight.co.uk

Visit www.taxesdoneright.co.uk

{kind=link}

{kind=link}

{kind=link}