Director’s Loan Account – The Silent Tax Trap

February 17, 2026

ATED Explained: Is Your Limited Company Owing Annual Property Tax?

February 19, 2026

Many company directors focus on profits, dividends and reducing their tax bill.

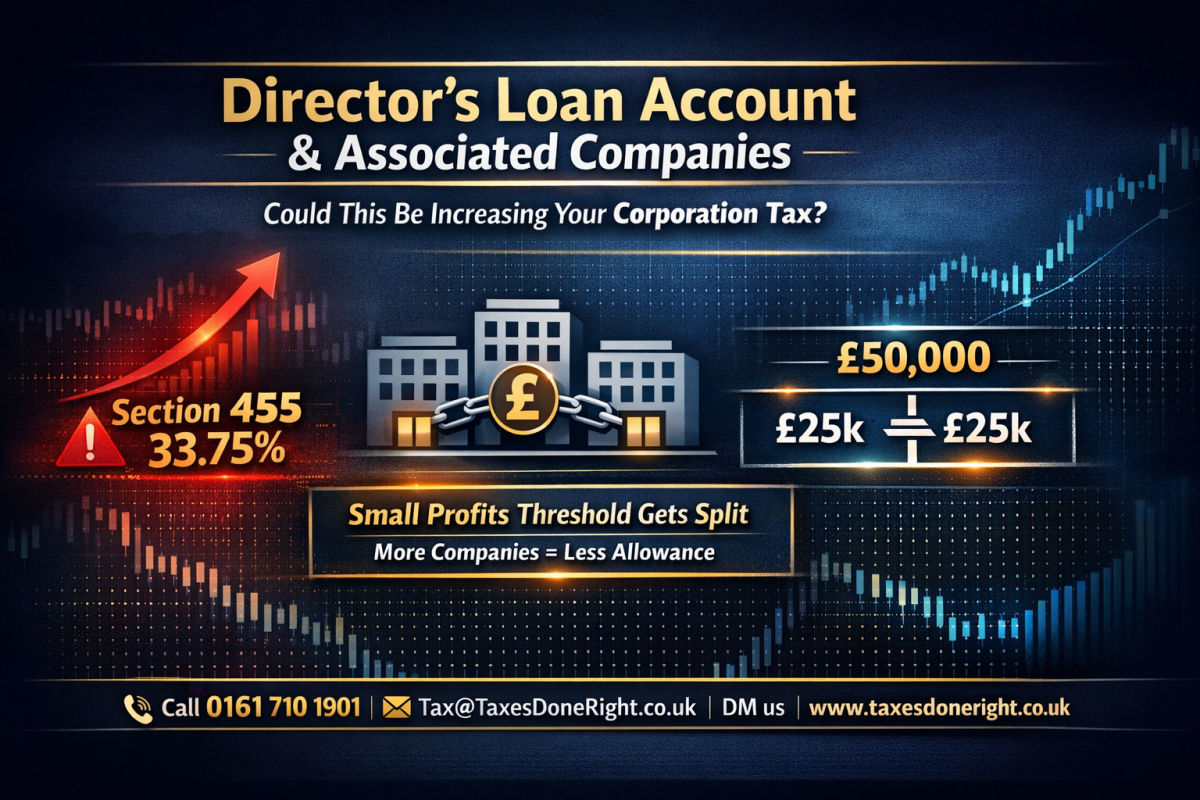

But two areas often overlooked can quietly increase your Corporation Tax:

• Your Director’s Loan Account (DLA)

• Whether your companies are classed as associated companies

When combined, these can significantly increase your tax exposure.

What Is a Director’s Loan Account?

A Director’s Loan Account records money you take from the company that is not salary, dividends, or expense reimbursements.

If you withdraw more than you put in, your DLA becomes overdrawn.

If that balance is not repaid within nine months of the company’s year end, the company must pay Section 455 tax at 33.75%.

Although this tax can be reclaimed once the loan is repaid, it creates a cash flow issue and ties up company funds.

There can also be:

• Benefit in kind charges if the loan exceeds £10,000

• Personal tax on the benefit

• Additional reporting requirements

On its own, this is manageable. But the bigger issue comes when you have more than one company.

What Are Associated Companies?

Two companies are associated if:

• They are under common control

• Or the same person or group of people control them

From April 2023 onwards, associated companies must share Corporation Tax thresholds.

That means:

• The £50,000 small profits threshold is divided

• The £250,000 upper threshold is also divided

If you own two companies, each only gets:

• £25,000 at the small profits rate

• £125,000 before reaching the main rate

Three companies? The thresholds are split three ways.

This means profits move into the higher Corporation Tax rate much sooner.

Why This Can Increase Your Tax Bill

Now combine:

- Reduced Corporation Tax thresholds due to associated companies

- An overdrawn Director’s Loan Account triggering Section 455 tax

The result?

• Higher Corporation Tax sooner

• 33.75% Section 455 tax on unpaid loans

• Possible benefit in kind tax

• Cash flow pressure

Many directors unknowingly create this situation by:

• Setting up multiple companies for different projects

• Using one company to fund another

• Taking informal withdrawals without declaring dividends

Without proper planning, the structure itself increases your tax liability.

Example Scenario

You own two limited companies.

Each makes £60,000 profit.

Because they are associated, the £50,000 small profits band is split. Each company only benefits from £25,000 at the lower rate.

The remaining £35,000 is taxed at a higher marginal rate.

Now add an overdrawn Director’s Loan Account of £40,000 not repaid within nine months.

The company must pay £13,500 in Section 455 tax.

This is where directors start to feel the squeeze.

What Should You Do?

If you:

• Run multiple limited companies

• Move money between companies

• Regularly withdraw funds

• Have an overdrawn Director’s Loan Account

You should review your structure urgently.

In some cases, restructuring or adjusting remuneration strategy can significantly reduce tax exposure.

Need Help Reviewing Your Structure?

At Taxes Done Right Ltd, we specialise in advising directors on:

• Director’s Loan Account planning

• Associated company rules

• Tax efficient profit extraction

• Corporation Tax mitigation strategies

{kind=link}

{kind=link}

{kind=link}