Companies House Fee Increase from February 2026 – What Businesses Need to Know

January 18, 2026

When Should You Register for Self‑Assessment?

January 20, 2026

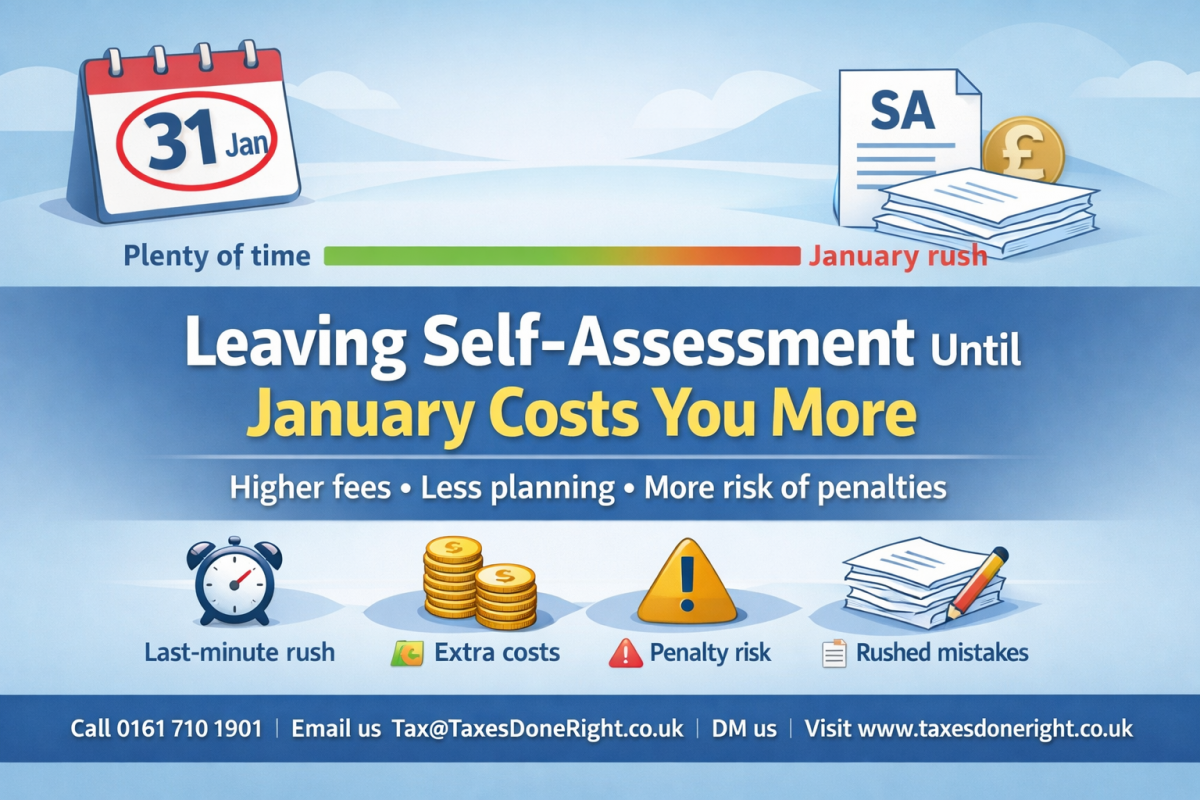

Every year, the Self-Assessment deadline lands on 31 January, and every year thousands of people leave it until the last minute. If you are tempted to do the same, it is worth knowing this: leaving your return until January often costs more than just stress. It can increase your accountant’s fees, reduce the time you have to plan your tax bill, and make penalties and interest far more likely if anything goes wrong.

1) You lose time to plan your tax bill properly

If you get your figures done early, you have options. You can review profit levels, pension contributions, charitable donations, allowable expenses, and whether any income can be timed better. In January, you are usually just trying to file on time. That means missed planning opportunities that could have reduced your tax legally, or at least helped you spread the cost more sensibly.

2) You risk paying more in accountant fees

January is the busiest month for tax advisers. If you contact an accountant late, you may face higher “rush” fees, or you may struggle to get a slot at all. Even if you already have an accountant, late paperwork means more chasing, less time to check, and more work done under pressure. That pressure often translates into higher costs.

3) Mistakes become more likely (and mistakes cost money)

Rushing increases the chance of missed expenses, incorrect figures, or forgetting income sources such as bank interest, dividends, side income, or property details. A small error can lead to an amended return, extra professional time, and sometimes HMRC queries. A return done calmly in good time is usually cheaper and more accurate.

4) You increase the chance of penalties

If you miss the deadline, HMRC issues an automatic £100 late filing penalty straight away. After that, daily penalties can apply, followed by further fixed penalties and tax-geared penalties if the delay continues. Even if you file on time, a late payment can still trigger interest and late payment penalties. January leaves you very little room for any unexpected delays.

5) You can end up paying tax later than needed and still feel broke

Many people assume doing the return in January means paying later, but the payment date is the same whether you file in April or January. The difference is that early filers can budget, set money aside monthly, and avoid the January financial shock. Leaving it late often means paying at the same time, but without preparation.

6) You may miss out on support if HMRC systems are busy

As the deadline approaches, HMRC phone lines and online services can be stretched. If you need a UTR, need to reset a Government Gateway login, or need information from HMRC, waiting until January can create avoidable delays and stress.

A simple way to avoid the January scramble

Aim to have your records ready by late summer or early autumn. That gives you enough time to fix gaps, confirm income figures, and calculate the tax in a way that supports sensible cashflow. Even if you do not want to file immediately, knowing your likely bill early is one of the best financial planning moves you can make.

Final thoughts

Leaving Self-Assessment until January rarely saves money. In most cases it increases cost, stress, and the chance of penalties. Filing early gives you time to plan, time to budget, and time to get it right.

Call: 0161 710 1901

Email: Tax@TaxesDoneRight.co.uk

DM us

Visit: www.taxesdoneright.co.uk

{kind=link}

{kind=link}

{kind=link}