Limited Cost Trader Rules Explained And Why They Catch People Out

April 30, 2026

VAT Registration Exception Explained (Avoid Costly Mistakes When Applying to HMRC)

May 1, 2026

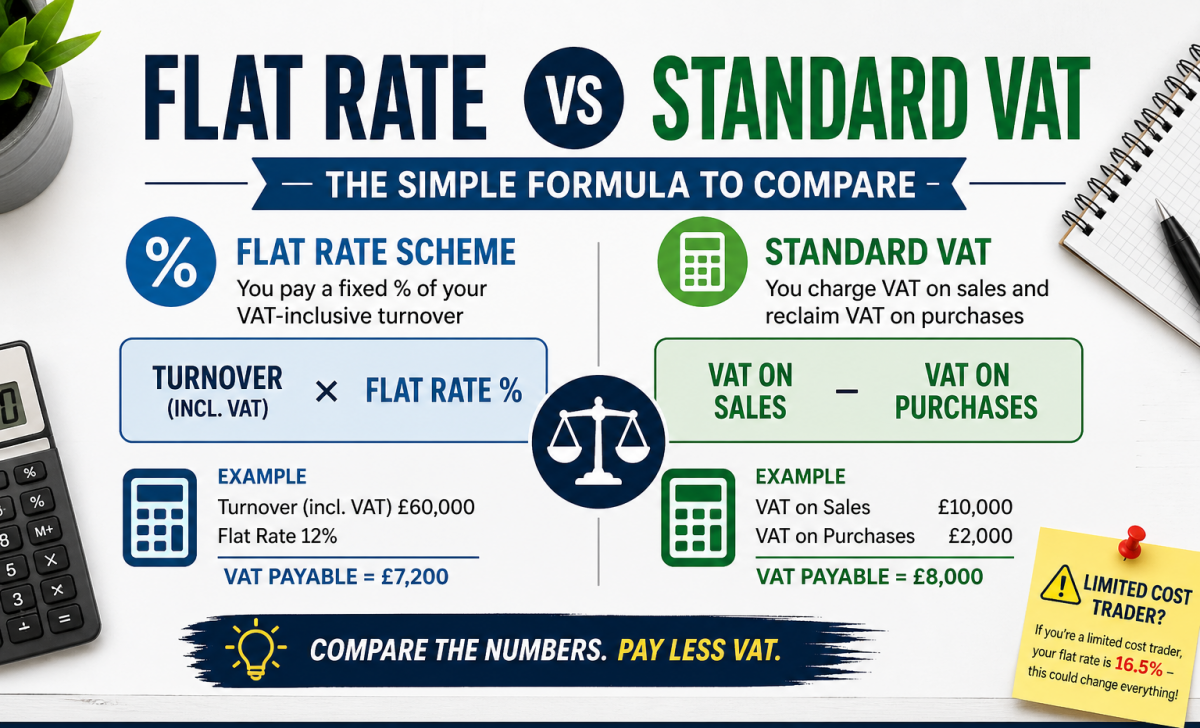

Choosing between the VAT Flat Rate Scheme and Standard VAT isn’t about guesswork. There’s a simple way to compare them side by side — and it can save (or cost) you thousands.

Step 1: Understand the Key Difference

- Flat Rate Scheme (FRS): You pay a fixed % of your gross (VAT-inclusive) turnover to HMRC

- Standard VAT: You charge VAT on sales and reclaim VAT on purchases

Step 2: Use This Simple Comparison Formula

Flat Rate VAT payable:

Turnover (incl. VAT) × Flat Rate %

Standard VAT payable:

VAT on sales – VAT on purchases

Step 3: Quick Worked Example

Let’s say:

- Turnover (excl. VAT): £50,000

- VAT charged (20%): £10,000

- Total income (incl. VAT): £60,000

- Purchases (incl. VAT): £12,000 (VAT element = £2,000)

Flat Rate Scheme (e.g. 12%):

£60,000 × 12% = £7,200 payable to HMRC

Standard VAT:

£10,000 (output VAT) – £2,000 (input VAT) = £8,000 payable

In this case, Flat Rate saves £800

Step 4: The Hidden Trap – Limited Cost Trader

If you’re classed as a limited cost trader, your flat rate jumps to 16.5%.

Using the same example:

£60,000 × 16.5% = £9,900

Now you’re £1,900 worse off than Standard VAT

Step 5: When Flat Rate Works Best

Flat Rate is usually beneficial if:

- You have low VATable expenses

- You’re not a limited cost trader

- Your industry flat rate % is relatively low

Step 6: When Standard VAT is Better

Standard VAT tends to win if:

- You have high costs with reclaimable VAT

- You regularly buy materials, stock, or equipment

- You fall into the limited cost trader rules

Final Thought

Don’t assume one scheme is always better. The right choice depends on your numbers — and they can change as your business grows.

A quick calculation using the formula above can highlight if you’re overpaying.

If you want us to run the numbers properly for your business:

📞 Call: 0161 710 1901

📧 Email: Tax@TaxesDoneRight.co.uk

Dm Us:

www.taxesdoneright.co.uk

{kind=link}

{kind=link}

{kind=link}