Trivial Benefits Explained – How Directors Can Take Tax-Free Perks

May 8, 2026

Making Tax Digital Is Now in Full Swing With Force

May 12, 2026

Why Most Buy-to-Let Landlords Do Not Charge VAT

The starting point is that residential rental income is generally exempt from VAT in the UK. This means Buy-to-Let Landlords renting out residential properties on standard assured shorthold tenancies usually do not charge VAT to tenants.

Because the income is VAT exempt rather than zero-rated, landlords also cannot normally reclaim VAT on related expenses.

For example, if a landlord pays VAT on:

- Letting agent fees

- Accountancy fees

- Repairs and maintenance

- Furniture purchases

- Insurance-related services

- Contractor invoices

that VAT normally becomes an additional cost to the landlord.

This is one of the key areas many Buy-to-Let Landlords misunderstand. Although no VAT is charged to tenants, VAT can still significantly affect profitability because input VAT recovery is often restricted.

When Buy-to-Let Landlords May Need VAT Registration

There are several scenarios where Buy-to-Let Landlords may need to consider VAT registration.

Commercial Property Income

If a landlord also rents out commercial property, the VAT position changes significantly.

Commercial property rental income is normally exempt from VAT by default, but landlords can choose to apply an “Option to Tax”. This allows VAT to be charged on rent and potentially enables VAT recovery on related expenses and refurbishment costs.

This is common where:

- Offices are rented out

- Shops or retail units are owned

- Warehouses are leased

- Mixed-use properties exist

- Commercial conversions are undertaken

If taxable turnover exceeds the VAT registration threshold, registration may become compulsory.

Buy-to-Let Landlords and Serviced Accommodation

Serviced accommodation is another major area where Buy-to-Let Landlords can accidentally trigger VAT registration.

Unlike standard residential lets, serviced accommodation can be treated more like hotel or holiday accommodation for VAT purposes.

This often applies where landlords provide:

- Short-term stays

- Cleaning services

- Linen changes

- Guest-style accommodation

- Airbnb-style lettings

Income from these activities is generally taxable for VAT purposes.

This means Buy-to-Let Landlords operating serviced accommodation businesses may need to register for VAT once taxable turnover exceeds the VAT threshold.

Many landlords expanding into short-term lets fail to realise this until turnover has already passed the registration limit.

The VAT Registration Threshold

The VAT registration threshold changes periodically, so landlords should always check the latest HMRC guidance.

If taxable turnover exceeds the threshold within a rolling 12-month period, VAT registration may become mandatory.

Use our interactive calculator to see where you stand. VAT Calculator

Importantly, exempt residential rental income does not normally count towards taxable turnover for VAT registration purposes.

However, taxable activities such as:

- Serviced accommodation

- Commercial property income

- Property management services

- Consultancy or sourcing businesses

can count towards the threshold.

Many Buy-to-Let Landlords operate multiple income streams and fail to separate exempt and taxable activities correctly.

Can Buy-to-Let Landlords Register for VAT Voluntarily?

Yes, Buy-to-Let Landlords can sometimes register voluntarily for VAT, but whether this is beneficial depends on the circumstances.

Voluntary registration may make sense where:

- Significant refurbishment costs are incurred

- Commercial property is involved

- Most customers are VAT-registered businesses

- Large VAT expenses need recovering

However, voluntary registration can also create additional administration and may increase costs for non-VAT-registered tenants.

For purely residential property portfolios, voluntary VAT registration is often not beneficial because residential rents remain exempt.

Buy-to-Let Landlords and VAT on Property Purchases

Another area of confusion involves VAT on property purchases.

Most residential property purchases are exempt from VAT, but commercial properties can sometimes include VAT depending on whether an Option to Tax has been applied.

This becomes especially important when Buy-to-Let Landlords purchase:

- Mixed-use buildings

- Commercial premises

- Semi-commercial investments

- Development opportunities

Failing to identify VAT correctly during acquisition can create unexpected costs worth tens of thousands of pounds.

Partial Exemption Rules for Buy-to-Let Landlords

Some Buy-to-Let Landlords operate businesses containing both exempt and taxable supplies.

For example:

- Residential rentals alongside serviced accommodation

- Residential property with commercial units

- Property investment plus consultancy services

In these situations, partial exemption rules may apply.

This area becomes highly technical because landlords may only recover a proportion of VAT on shared expenses.

Calculating recoverable VAT incorrectly can lead to HMRC enquiries and repayment demands.

Common VAT Mistakes Buy-to-Let Landlords Make

There are several recurring VAT mistakes made by Buy-to-Let Landlords:

Assuming VAT Never Applies to Property

Many landlords wrongly believe VAT has no relevance to residential property businesses.

Ignoring Airbnb and Short-Term Let Rules

Short-term accommodation can create taxable supplies even where landlords previously operated traditional rentals.

Forgetting About Mixed Businesses

Property businesses often expand into sourcing, management or consultancy services which may all have different VAT treatment.

Not Reviewing Commercial Leases Properly

Commercial property transactions can contain hidden VAT implications.

Missing the VAT Registration Threshold

Some landlords exceed the threshold gradually and only discover the issue after HMRC intervention.

Should Buy-to-Let Landlords Speak to an Accountant?

VAT and property is one of the most complex areas of UK taxation.

Buy-to-Let Landlords should strongly consider professional advice if they:

- Operate serviced accommodation

- Own commercial property

- Have mixed-use buildings

- Are approaching the VAT threshold

- Plan major refurbishments

- Are considering an Option to Tax

- Run multiple property-related businesses

Proper planning can improve cash flow, avoid penalties and prevent expensive mistakes.

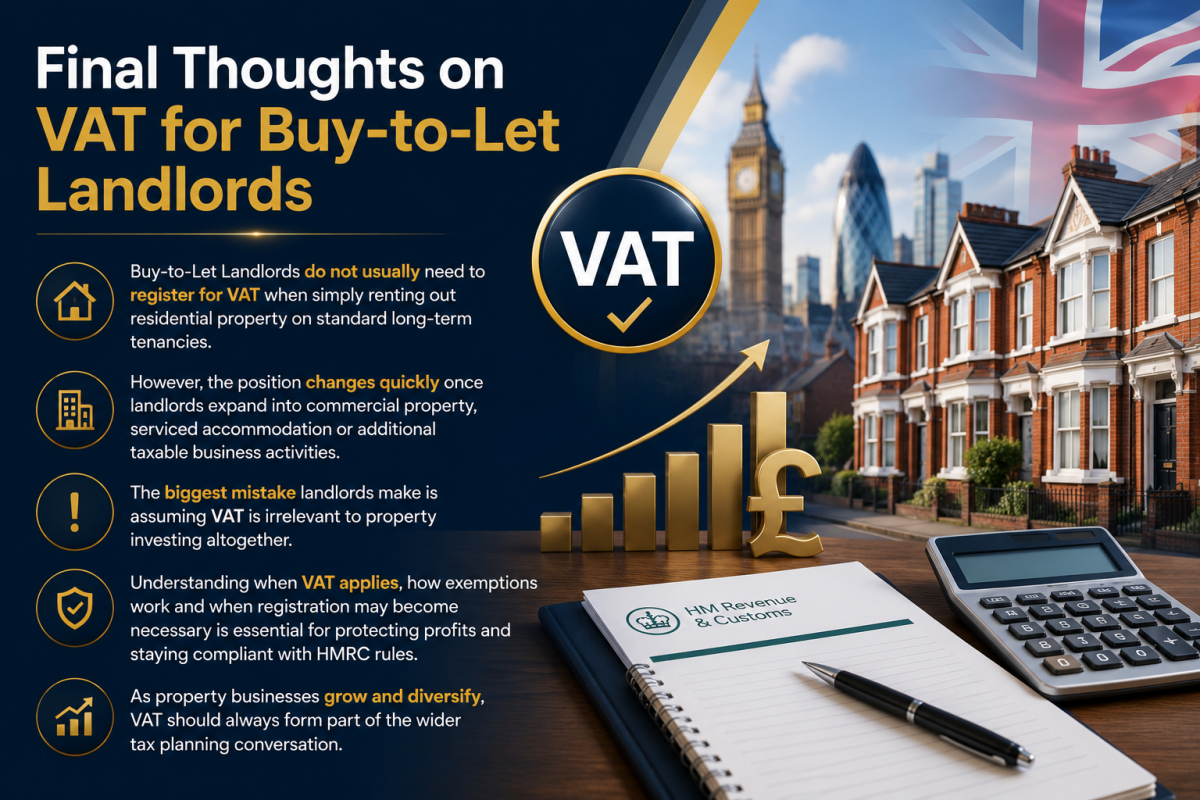

Final Thoughts on VAT for Buy-to-Let Landlords

Buy-to-Let Landlords do not usually need to register for VAT when simply renting out residential property on standard long-term tenancies.

However, the position changes quickly once landlords expand into commercial property, serviced accommodation or additional taxable business activities.

The biggest mistake landlords make is assuming VAT is irrelevant to property investing altogether.

Understanding when VAT applies, how exemptions work and when registration may become necessary is essential for protecting profits and staying compliant with HMRC rules.

As property businesses grow and diversify, VAT should always form part of the wider tax planning conversation.

Need clarity on your situation?

📞 Call 0161 710 1901

📧 Email Tax@TaxesDoneRight.co.uk

{kind=link}

{kind=link}

{kind=link}