How HMRC Matches Property Income to Land Registry Data

January 27, 2026

Why HMRC Can Amend Your Self-Assessment Without Asking You First

January 29, 2026

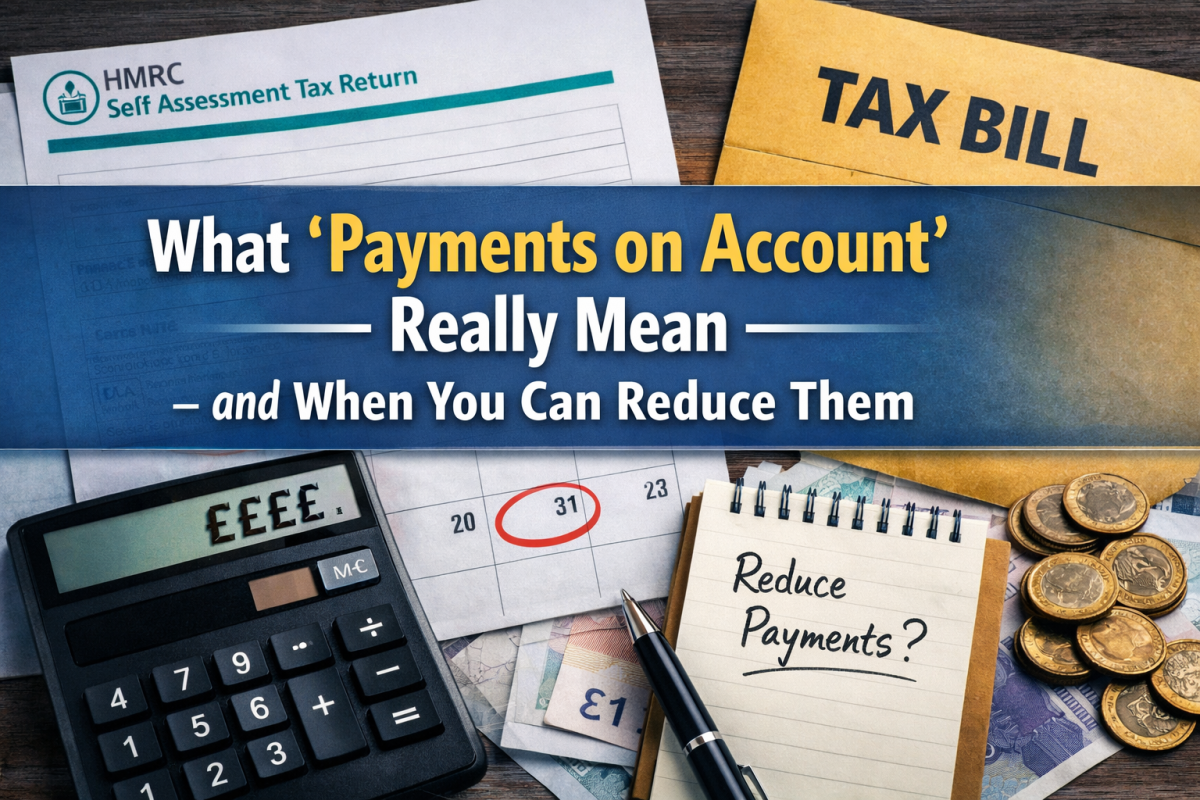

If you’ve ever submitted a Self Assessment tax return and been surprised by a much larger bill than expected, chances are Payments on Account are the reason.

They’re one of the most misunderstood parts of the UK tax system, especially for sole traders, landlords, and company directors with untaxed income. In this guide, we’ll explain what Payments on Account actually are, why HMRC ask for them, and when you’re allowed to reduce them.

What Are Payments on Account?

Payments on Account are advance payments towards your next tax bill.

Instead of paying all of your tax after the end of the tax year, HMRC ask many taxpayers to pay tax in advance, based on the previous year’s bill.

Each year, you normally make:

- Two advance payments, and

- One balancing payment

When Are Payments on Account Due?

If they apply to you, HMRC will ask for:

- 31 January – First Payment on Account (50%)

- 31 July – Second Payment on Account (50%)

Then, when you submit your next tax return, you pay:

- A balancing payment on 31 January to settle any difference

Who Has to Pay Payments on Account?

You usually will have to pay Payments on Account if:

- Your Self Assessment tax bill is over £1,000, and

- Less than 80% of your tax was collected at source (for example via PAYE)

This often affects:

- Sole traders

- Landlords

- Directors taking dividends

- Individuals with multiple income sources

You won’t usually pay them if you’re fully taxed under PAYE.

Why Does HMRC Do This?

HMRC’s logic is simple:

they don’t want to wait up to 22 months to collect tax on ongoing income.

So instead, they:

- Assume your income will be similar next year, and

- Ask you to pay tax in advance

The problem is that real life doesn’t always work like that.

Why Your January Bill Feels So High

Many people are shocked in January because they’re asked to pay:

- The balancing payment for the year just ended, plus

- The first Payment on Account for the new year

This can feel like paying 150% of your tax bill at once, even though part of it is for the future.

When Can You Reduce Payments on Account?

You’re allowed to reduce your Payments on Account if you genuinely expect your tax bill to be lower.

Common valid reasons include:

- Your income has dropped

- You stopped trading or became employed

- Rental income has reduced or a property was sold

- Higher expenses or reliefs are expected

- One-off income inflated last year’s tax bill

This must be based on a reasonable estimate, not guesswork.

How Do You Reduce Them?

You can apply to reduce Payments on Account:

- Through your HMRC online account, or

- Via your Self Assessment tax return, or

- With professional help to ensure it’s done correctly

If reduced properly, this can significantly ease January and July cash-flow pressure.

Important Warning: Don’t Reduce Them Lightly

If you reduce Payments on Account too much and end up owing more tax:

- HMRC will charge interest on the underpaid amount

- Penalties can apply if the reduction was careless or unreasonable

This is why reductions should be calculated, documented, and justified.

Key Takeaway

Payments on Account are not extra tax – they’re advance payments.

But:

- They can seriously affect cash flow

- They don’t always reflect your real situation

- They can be reduced when done properly

If your income has changed, it’s worth reviewing them rather than blindly paying what HMRC asks.

Unsure If You’re Paying Too Much Tax in Advance?

If your income has dropped or changed, you may be overpaying HMRC through Payments on Account without realising it.

A proper review can:

- Check whether a reduction is valid

- Protect you from HMRC interest or penalties

- Improve cash flow in January and July

- Make sure you’re only paying what’s actually due

Get in touch today for a Payments on Account review and we’ll confirm whether a reduction is possible and handle it correctly on your behalf.

📞 Call: 0161 710 1901

📧 Email: Tax@TaxesDoneRight.co.uk

Dm Us:

TaxesDoneRight

{kind=link}

{kind=link}

{kind=link}