When Is the Right Time to Hire an Accountant for Your Small Business?

April 28, 2026

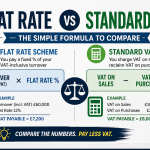

The Simple Formula to Compare Flat Rate vs Standard VAT

April 30, 2026

If you’re VAT registered and using (or considering) the Flat Rate Scheme, the “limited cost trader” rules are something you cannot afford to ignore. They sound technical, but in practice they can significantly increase the VAT you pay — often unexpectedly.

What is a Limited Cost Trader?

Under HM Revenue & Customs rules, a business is classed as a limited cost trader if it spends very little on relevant goods.

In simple terms, you fall into this category if:

- Your spend on goods is less than 2% of your VAT-inclusive turnover, OR

- Your spend on goods is less than £1,000 per year (if that’s higher than 2%)

If either applies, you’re caught by the rules.

Why does it matter?

If you are a limited cost trader, you must use a flat rate of 16.5%, regardless of your industry.

That’s the key issue.

Most businesses join the Flat Rate Scheme expecting a lower percentage (e.g. 10%, 12%, etc.), but once caught by these rules, that benefit disappears — and often reverses.

What counts as “goods”?

This is where many people get caught out.

Goods include:

- Physical items used in your business

- Stock you resell

- Materials you directly use

Goods do NOT include:

- Services (e.g. subcontractors, freelancers)

- Software subscriptions

- Rent, utilities, or phone bills

- Accountancy fees

- Vehicles, fuel, or capital assets

So even if you have high expenses overall, you can still be classed as a limited cost trader if most of your costs are services.

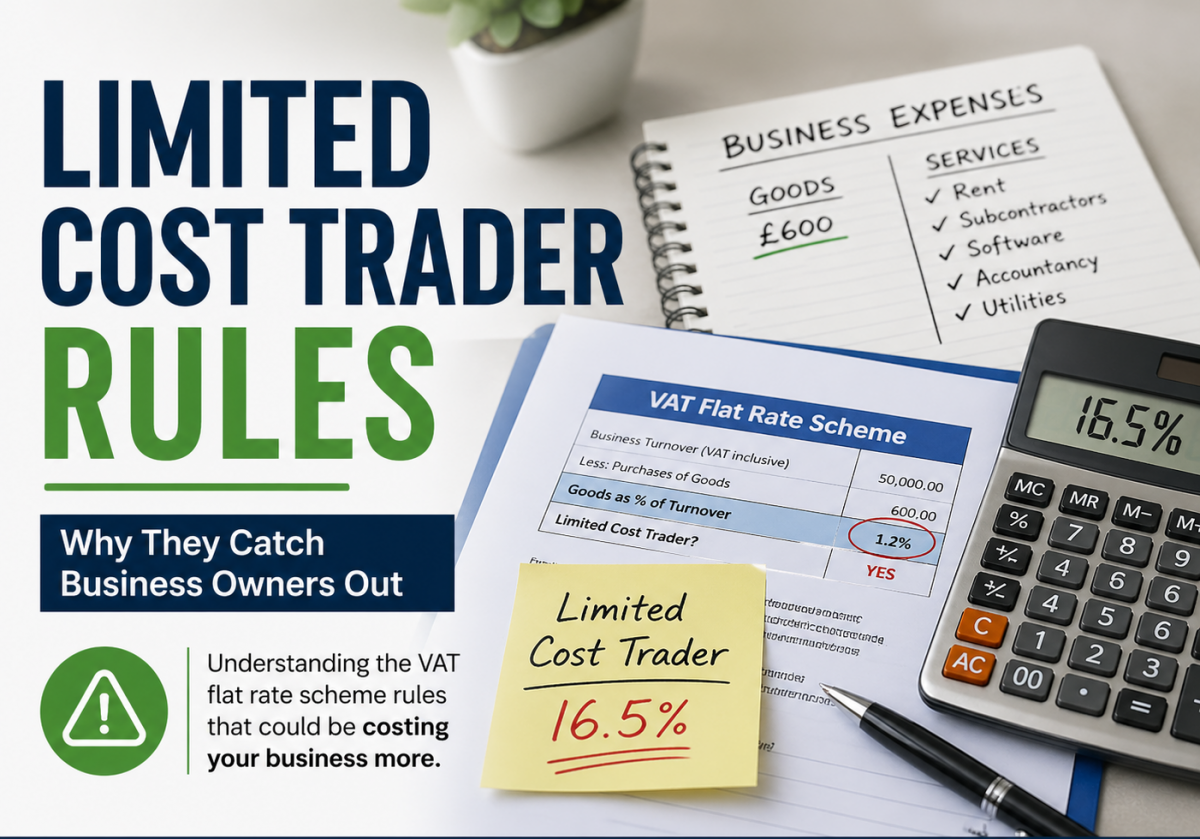

Example

Let’s say:

- Turnover (VAT inclusive): £50,000

- Spend on goods: £600

2% of £50,000 = £1,000

Your goods spend (£600) is below both thresholds → you are a limited cost trader.

This means you must apply 16.5%, which could result in paying more VAT than using standard VAT accounting.

Why people get caught out

There are a few common reasons:

1. Misunderstanding “costs”

Many assume all expenses count. They don’t. Only specific goods qualify.

2. Service-based businesses

Consultants, contractors, and digital businesses often have minimal goods — so they fall into this rule automatically.

3. Not reviewing regularly

Your status can change. If your spending pattern shifts, your VAT treatment might need to change too.

4. Blindly choosing Flat Rate Scheme

It’s not always beneficial — especially under these rules.

Should you avoid the Flat Rate Scheme?

Not necessarily.

It still works well for some businesses, particularly those with low admin needs and consistent margins. But if you’re a limited cost trader, you need to compare it carefully against standard VAT accounting.

In many cases, standard VAT may be more efficient.

Key takeaway

The limited cost trader rule is one of the most misunderstood VAT traps. It often turns what looks like a simple, tax-saving scheme into a more expensive option.

Before choosing (or continuing with) the Flat Rate Scheme, it’s worth reviewing your numbers properly.

If you’re unsure whether this applies to you, or if you’re currently overpaying VAT, it’s worth getting it checked.

📞Call: 0161 710 1901

📧Email: Tax@TaxesDoneRight.co.uk

Dm Us:

www.taxesdoneright.co.uk

{kind=link}

{kind=link}

{kind=link}